At the time when the cryptocurrency industry has recorded a loss of more than $30 billion, two Yale economists believe traders can strongly forecast the volatile market using “potential predictors for cryptocurrency returns.”

Aleh Tsyvinski and Yukun Liu published a new study, titled “Risks and Returns of Cryptocurrency,” after researching factors that could accurately predict the cryptocurrency returns. The study found that cryptocurrencies have low exposure to the macroeconomic factors that usually influence stock, currency, and commodity markets. However, there are still some strategies that are common to both traditional and cryptocurrency price trends.

To find them, Tsyvinski and Liu analyzed the historical data of top coins, including Bitcoin, Ethereum, and Ripple, and eventually determine two key factors that could predict the market’s next trend. They are called “Momentum Effect” and “Investor Attention Effect”.

Momentum Effect: Up means Up, Down means Down

The Yale economists investigated the daily and weekly frequencies of Bitcoin, Ethereum, and Ripple price actions, and what they believe to be a meaningful tool to predict Bitcoin price trends – the “time-series cryptocurrency momentum.”

In general, the momentum effect compares trends with their timeframes. For instance, a substantial price weekly rally – over 20% – should be taken as a sign to purchase the cryptocurrency. A trader, then, should hold the asset for at least a week before selling it at a profitable margin. Similarly, an extended downside momentum – again weekly – should be taken as a sign to quickly exit the market, before the risk intensifies.

“Momentum is actually something simple,” Tsyvinski told CNBC. “If things go up, they continue to go up on average, and if things go down, they continue to go down.”

Investor Attention Effect: Social Trends

The Yale study constructed the deviation of Google Searches for the keywords “Bitcoin,” “Ripple,” and “Ethereuem” and compared the weekly outcome with their respective price data. The average increase in the social media queries for each asset indicated that the price of the asset will increase in the coming weeks.

Similarly, negative investor attention consorting with keywords like “bitcoin hack” predicted a decrease in price.

A Twitter-based research also assisted the study. Tsyvinski and Liu that the increase in the number of posts about Bitcoin on Twitter predicted an upside in the coming weeks.

“A one-standard-deviation increase in the Twitter post count for the word “Bitcoin” yields a 2.50 percent increase in the 1-week ahead Bitcoin returns,” the paper revealed.

Data Output of Bitcoin, Ethereum and Ripple

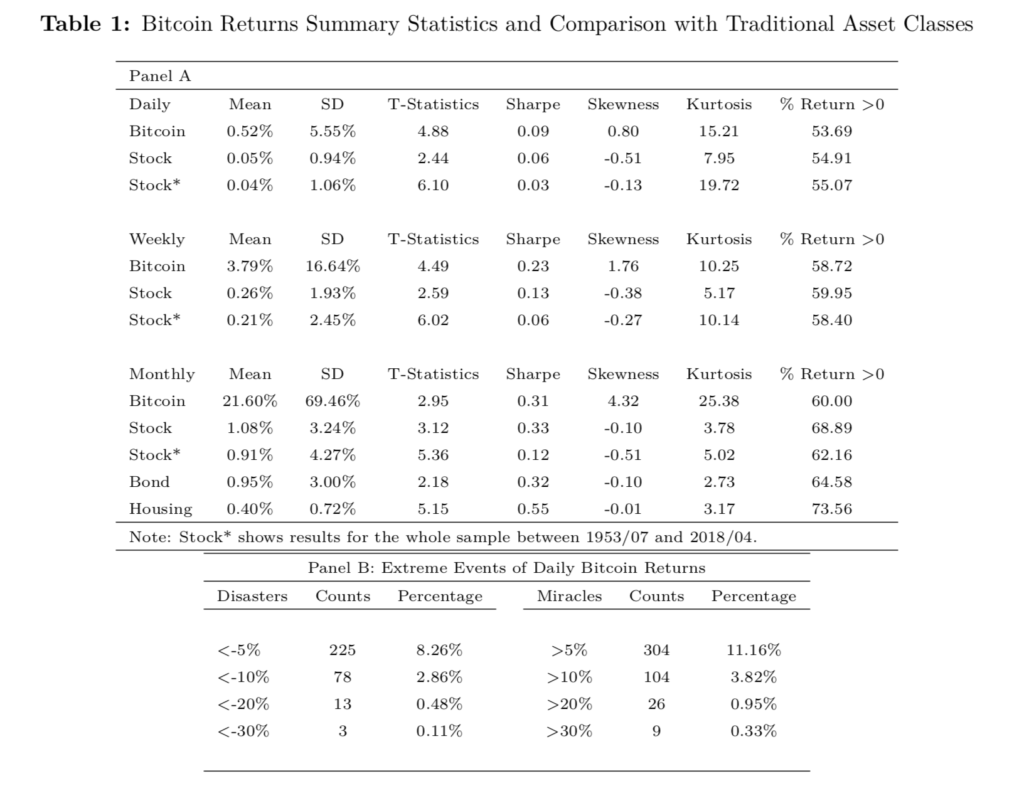

The study compared the statistics of Bitcoin on the daily, weekly, and monthly basis, and also compared to those of currencies, stocks, and commodities. It found that “at the daily frequency, the mean return [was]0.52 percent and the standard deviation [was]5.55 percent; at the weekly frequency, the mean return [was]3.79 percent and the standard deviation [was]16.64 percent; at the monthly frequency, the mean return [was]21.60 percent and the standard deviation [was]69.46 percent.”

Overall, the magnitude of the outcomes derived from Bitcoin statistics was higher than those for traditional asset classes.

As for Ripple and Ethereum, their returns had a higher mean return and standard deviation than those of Bitcoin. However, their Sharpe ratios, the average profit earned, was somewhat comparable to the Sharpe ratios of Bitcoin returns.

Featured image from Shutterstock.

Follow us on Telegram or subscribe to our newsletter here.

• Join CCN’s crypto community for $9.99 per month, click here.

• Want exclusive analysis and crypto insights from Hacked.com? Click here.

• Open Positions at CCN: Full Time and Part Time Journalists Wanted.

{kind=link}