In today’s market update, we delve into the significant developments that are shaping the financial landscape. From historically high U.S. stock valuations to a deteriorating labor market, we cover a range of topics that offer a comprehensive view of the market.

With valuations at historically high levels and a deteriorating labor market set to be the catalyst for this collapse, this is a terrible time to invest in U.S. stocks long-term. Current valuation levels for U.S. stocks are very high, and over a roughly ten-year period, valuation levels have a significant impact on determining investment returns. According to Bank of America, valuation levels explain 80% of stock market returns over 10 years.

John Hussman has provided an indicator for measuring overall market valuation. Hussman considers this to be the most accurate indicator he has found for predicting future market returns, with the indicator showing an annualized return of -5% for the S&P 500 over the next 12 years.

The Buffett indicator (ratio of total market capitalization to GDP) has far exceeded the level during the Internet bubble and is approaching the high in 2022. Additionally, the cyclically adjusted price-to-earnings ratio (CAPE ratio) surpassed 1929 levels and lagged only 1999 and 2021 levels.

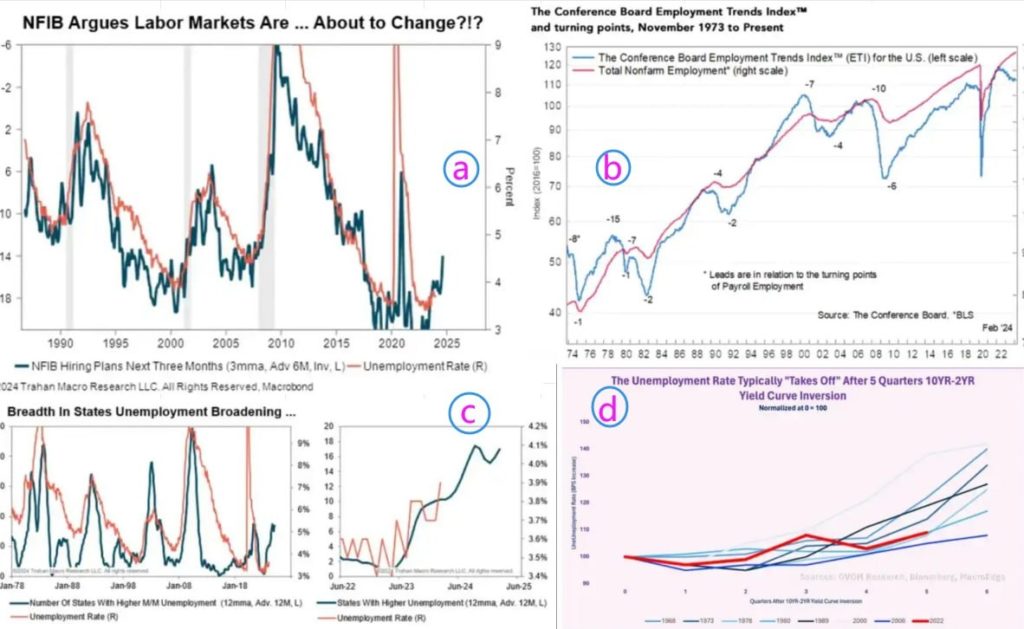

The trigger will be the weakness of the U.S. labor market and its subsequent economic recession, with several indicators indicating that the unemployment rate may rise in the coming months. The American Federation of Independent Business’s Recruiting Initiative Index’s three-month moving average is surging, signaling a possible rise in unemployment. The Conference Board’s Employment Trends Index has declined in recent years, which historically has meant trouble for U.S. nonfarm payrolls. The number of unemployment rates in various states in the United States is increasing rapidly, which means that the overall unemployment rate will continue to rise.

Unemployment typically begins to rise approximately five quarters after the U.S. Treasury yield curve inverts (using 10-year and 2-year U.S. Treasury yields). April marks the sixth quarter since the yield curve officially inverted, which is considered official when the curve remains inverted for three months.

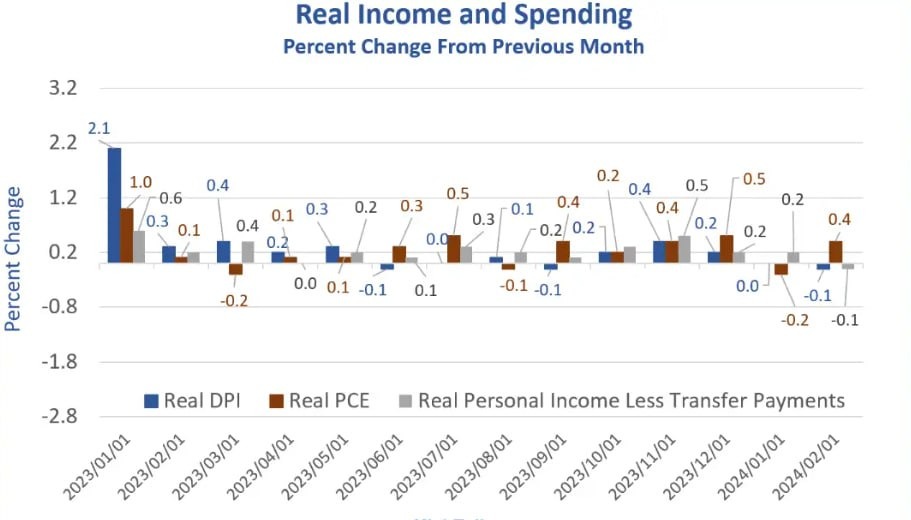

The U.S. unemployment rate has been rising slightly, from 3.4% in April 2023 to 3.9% in February 2024. According to the Sahm Rule, named after former Fed economist Claudia Sahm, the U.S. economy is effectively in recession once the three-month moving average of the unemployment rate rises 0.5% from the low of the past 12 months. The indicator has a perfect record of identifying recessions and currently stands at 0.27. This means that if the unemployment rate continues to rise, the U.S. economy will be getting closer to declaring a real-time recession according to Sam’s rule.

{kind=link}