The inability to quickly process Bitcoin payments finally showed its face in 2017 when prices were high. Not only that, but transaction costs for trading in the pioneer cryptocurrency were far from competitive. And yet, cryptocurrencies have still managed to capture the minds of many world leaders. The reason? In a world as financially-intertwined as ours, the ability to evade geopolitical sanctions is worth its weight in digital gold.

SWIFT Is Alive and Well

The great network of banks, exchanges, and payment providers can be equated to the success of conglomerates like SWIFT. With over 11,000 institutions in more than 200 countries being served, there is no real reason why governments wouldn’t side with the member-owned cooperative. The service has also just released a speedier gpi which allows for lightning-fast settlements within its network. In October 2018, the group explained that a transaction between Australia and China would only take 18 seconds.

For a bit of perspective, Statista reported that the average confirmation time for the Bitcoin network in November 2018 was 14.3 minutes. In December 2017, it averaged 2,322.

As reported by Breaker in November, similar innovations are also true for TransferWise and central banks are replacing payments rails to make way for real-time financial innovations. JP Konig of Breaker writes:

“The Bank of England, UK’s central bank, was one of the first off the mark in 2008 with its Faster Payments system. Since then, other central banks have built their own real-time retail payments systems. Sweden’s BiR opened in 2012, Singapore’s FAST in 2014, and Australia’s NPP in 2018. The European Central Bank is slowly rolling out SCT Instant while in the U.S., privately-owned The Clearing House’s Real-time Payment (RTP) is live.”

So, while crypto observers were busy pointing out the flaws in legacy financial systems, incumbents simply went ahead and upgraded. Still, others are unconvinced that there isn’t a place for Bitcoin. Nic Carter, a data scientist who’s earned his stripes in the world of cryptocurrencies, reminded audiences at Baltic Honeybadger 2018 that Bitcoin is responsible for moving “container ships, not parcels.” Similarly, $194 million was moved along Bitcoin’s blockchain for the cost of $0.01, further outlining the network’s large-scale capacities.

Bitcoin average transaction value: $3,000

VISA average transaction value: $81@nic__carter nailed this at #bh2018… Bitcoin is moving container ships, VISA is moving parcels.Keep that in mind when comparing daily transactions across different networks. pic.twitter.com/JZRp9CacyI

— Kevin Rooke (@kerooke) September 23, 2018

The above narrative is often talked about but still serves to explain the lengths cryptocurrencies will need to go if they have any chance of world domination. From this, another narrative emerges when considering the impossibility o actually toppling MasterCard and Visa. In the noose-like situation of the current bear market digital assets will most likely be absorbed and re-marketed as “finance 2.0.”

The community is demanding institutional adoption and, well, ApplePay is attractive enough, right?

Living in Marginalized Countries and Russia

Anywhere that a country has either launched a national cryptocurrency or is in the state of eternally mulling over such a project, is likely a country victim of “de-risking.” Oxfam defines the term as “financial institutions exiting relationships with and closing the accounts of clients considered ‘high risk.’ There is an observed trend toward de-risking of money service businesses, foreign embassies, nonprofit organizations, and correspondent banks, which has resulted in account closures in the US, the UK, and Australia.”

The reasons behind de-risking are naturally pretty cloudy and are subject to whoever is offended by a member state’s economic behavior. A region could be escorted out of the global economy due to low profitability as well, or updated standards of KYC/AML regulations. Once out, leaders are nearly powerless when it comes renegotiating their entry.

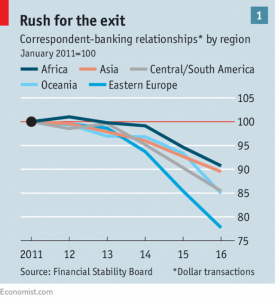

In the case of Latvia, a mass exodus between 2015 to 2017 following rumors of dirty money circulating between financial groups, left banks scrambling for alternatives. The Economist reported, “[Deutsche Bank] soon stopped serving half of Latvia’s lenders, and in March began dropping the rest, leaving them at risk of being unable to conduct dollar-denominated transactions, from paying remittances to financing trade.”

(Source: The Economist)

There is even a governing body called the Financial Action Task Force (FATF) who determines membership. And as fines for any whiff of financial illegibility sky-rocket, being on the wrong side of the group’s moral compass could spell catastrophe for your country.

In the case of Venezuala, Russia, Iran, the Central Africa Republic, Nicaragua, and others, many have been limited either by intercontinental sanctions or trading partners fears of misstepping. Belize and Liberia, for instance, have lost correspondent-banking services altogether. Cryptocurrencies, for better or worse, provide an alternative to this. In the very least, they offer breathing room for nations cast aside. Larger countries, such as Russia, are also looking for alternatives in the grand scheme of geopolitics.

In December 2018, Russia’s central bank sent out letters to five Russian banks and asked them to “prepare for tough scenarios” according to Russian news outlet UAWire. Specifically, many of the financial groups are at risk from being disconnected from the SWIFT network altogether. In the past, being neglected by American businesses has meant the collapse of more than a dozen Russian businesses.

For some, the American sanctions use the dollar as a tool of coercion which has serious effects on a country’s well-being. As Venezuela has also been on the receiving end of these sanctions, they have optimistically launched their native cryptocurrency, the Petro. Iran and Russia are also considering the use of a native cryptocurrency to outwit potential de-risking.

Unfortunately, the world’s first nationalized cryptocurrency is painting a rather bleak picture for Maduro and his administration.

Blockchain Technology, not Bitcoin

An unregulated, sovereign money with no central point of control is the last thing on a government’s Christmas list. A private, centralized database that can only be changed by staking participants, however, is highly attractive. This dichotomy is ultimately what bankers mean when they chant blockchain over crypto.

It is also in this phrase that observers can see how crypto will die in the hands of Internet hobbyists and be reborn by the JP Morgans of the world.

As countries hurdle towards cashless societies, it’s only a matter of time before a “better” money arrives to meet citizens’ digital lifestyles. The difficult prediction to parse from the above certainty is whether that money will continue to carry the infamous “B” or if SWIFT will sweep up the technology in a quarterly update.

Category: Bitcoin, Blockchain, Ethereum, Finance, News, Platform, Tech

Tags: bitcoin, censorship, cryptocurrency, digital tokens, FATF, resistance, sanctions

{kind=link}