Summary

Facebook’s Project Libra resolves three key challenges that are currently plaguing existing cryptocurrencies from widespread adoption.

Unlike the speculative nature of conventional cryptocurrencies, Libra provides a roadmap and business model in applying blockchain technology to boost Facebook’s top and bottom line.

The strength of Facebook’s core business provides value investors with an adequate margin of safety even under the scenario where Project Libra fails to see the light of day.

Editor’s note: Seeking Alpha is proud to welcome Roger Teoh as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Essential. Click here to find out more »

Blockchain, the underlying technology powering cryptocurrencies such as Bitcoin (BTC-USD) and Ethereum (ETH-USD), has attracted the capital of investors, speculators, and institutions alike as it holds tremendous potential in reshaping and disrupting the financial and banking industry. Last week, Facebook (FB) jumped into the fray and unveiled its plans for a new global digital currency, Libra, scheduled to launch in the first half of 2020.

While many articles have since been written in this platform on Facebook’s Libra, this article will focus on two topics that are yet to be discussed: “(1)” the fundamental differences between investing in Facebook versus conventional cryptocurrencies for an investor who wants exposure to the blockchain industry and “(2)” the margin of safety that Facebook’s stock currently exhibits should its venture into cryptocurrencies fail at the first regulatory hurdle.

Facebook’s Libra intends to resolve key challenges that are currently plaguing existing cryptocurrencies from gaining public support and widespread adoption, in particular, price volatility, scalability to handle large transaction volumes and simplicity of use:

Firstly, to establish a low-volatility cryptocurrency, Libra will be backed by a reserve of real assets such as short-term government securities and currencies in the form of bank deposits. The value of one Libra depends on the underlying value of these basket of assets. We also note that a stable source of income from these reserve assets (source: Facebook Libra’s Whitepaper) could give Libra an advantage relative to other cryptocurrencies that are currently in development. Unlike conventional cryptocurrencies which typically rely on an Initial Coin Offering “(ICO”) and one-off funding from venture capital, the self-funding nature of Libra implies that it is able to sustainably fund its research & development costs to continuously improve its blockchain network over time.

Secondly, trade-offs have to be made between structuring the blockchain network as a centralised or decentralised system. For example, a highly decentralised blockchain network such as Bitcoin and Ethereum provides many advantages but is constrained by the number of transactions that can be processed, while centralised systems are typically more efficient and have a higher transaction throughput. For Libra, the scalability issue to handle large transaction volumes is resolved by tentatively structuring Libra as a centralised blockchain. At present day, Facebook has partnered with the likes of Mastercard (MA), PayPal (PYPL), Visa (V), eBay (EBAY), Lyft (LYFT), Uber (UBER), Spotify (SPOT), and 18 other entities to govern and operate the Libra blockchain. Facebook aims to have over 100 launch partners on board the Libra Association to govern the cryptocurrency at its scheduled launch next year, before transitioning towards a more decentralised structure over the next five years as blockchain technology improves (source: Facebook Libra’s Whitepaper).

Thirdly, Facebook will also be launching a subsidiary company, Calibra, to develop a new digital wallet with the intention to simplify and improve the user experience of blockchain technology for ease of adoption for the general public. By integrating Calibra with Facebook’s core apps, it intends to provide new payment and financial services within Facebook and Instagram (e-commerce and ad purchases), as well as the monetisation of WhatsApp and Messenger with functions such as peer to peer and business payments similar to Tencent’s (OTCPK:TCEHY) WeChat.

Given these differences relative to conventional cryptocurrencies in terms of its low volatility, centralisation, and regulatory compliance, Libra caters to different types of communities in favour of the average Joe rather than cryptocurrency enthusiasts that champion for complete decentralisation and independence from the current financial system. These characteristics imply that future users are more inclined to utilise Libra as a currency to facilitate financial transactions rather than using it as an “investment” or speculative vehicle for capital gains.

Therefore, speculative theories put forward by cryptocurrency enthusiasts in hoping that Libra will be a positive catalyst to facilitate mass adoption towards conventional cryptocurrencies (and eventually boosting their coin prices) are unsubstantiated and bound to be disappointed. Unlike conventional cryptocurrencies, which according to the opinion of Warren Buffett rely on the greater fool theory for its price to appreciate, Libra provides a roadmap and a business model in applying blockchain technology to grow Facebook’s top and bottom line.

What happens to Facebook’s Stock Price should Libra fail?

We used a pro forma methodology to estimate Facebook’s intrinsic value by excluding any future revenue streams outside its core advertising business to determine any possible downside to Facebook’s stock price should Project Libra fails at the first regulatory hurdle. Given the simplicity of Facebook’s business model, three simple equations are used to simulate Facebook’s EPS growth that solely originates from its core advertising business up until the year 2025:

Total Revenue = Monthly Active User “(MAU)” × Average Revenue Per User “(ARPU)”

Operating Profit = Total Revenue × Operating Margin

Net Profit = Operating Profit × Effective Tax Rate

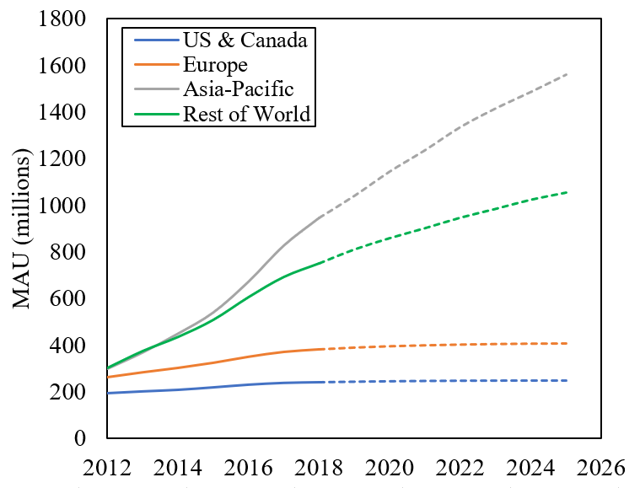

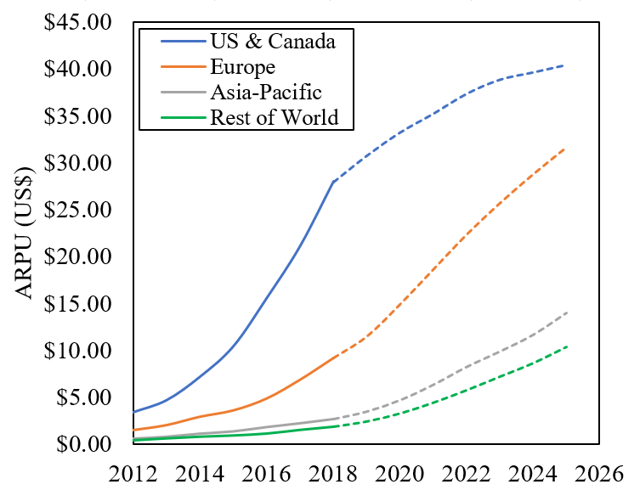

Figures 1 and 2 show the historical (solid lines) and forecasted data (dash lines) for the MAU and ARPU, while table 1 below summarises these data to arrive at Facebook’s intrinsic value:

Figures 1 & 2: Facebook’s historical and projected MAU and APRU. These figures were developed by the author, with its historical data obtained from Facebook’s Annual Reports (2012 to 2018).

The major assumptions are as follows:

- Facebook’s MAU in North America and Europe grow at less than 1% annually, while Asia-Pacific and the Rest of World continues to expand

- Over the next 10 years, the ARPU in Asia-Pacific (US$2.68/user in 2018) and the Rest of World (US$1.88/user in 2018) catches up to Europe’s ARPU today (US$9.17/user, 2018), while Europe’s ARPU gradually catches up to North America’s ARPU today (US$27.99/user in 2018)

- The operating margin gradually reduces from 45.5% (2018) to 30% (2025)

- The effective tax rate remains constant at 21%, barring any introduction of new taxes around digital services

- A Price-Earnings (P/E) multiple of 20 and a discount rate of 9.5%

Even under the absence of new revenue streams from e-Commerce (i.e. Instagram Check Out, currently on beta) or from Project Libra, as well as the exclusion of the positive effects of share buybacks, the above methodology gives an intrinsic value of US$214/share for Facebook, exhibiting a margin of safety of approximately 10%.

Ultimately, the strength in Facebook’s core business model of online advertising puts the company in a very good position to experiment around with a game-changing “high risk and high returns” strategy without introducing any downside risk to its stock price. Facebook’s Libra project can afford to fail, and the stock’s intrinsic value would still be worth US$214.

On the other hand, should any speculative cryptocurrencies (or Altcoins) fail, they would instantly be worth nothing, which represents a substantial risk of a permanent loss of capital. While some of the existing cryptocurrencies in development certainly have the potential to change the world for the better, their speculative nature, in particular, the lack of a roadmap to achieve profitability as well as the absence of a sound methodology to estimate their intrinsic value implies that these projects cannot be classified as “investments” at its current form.

As quoted in Warren Buffett’s biography (The Snowball: Warren Buffett and the Business of Life by Alice Schroeder):

Business history was replete with new technologies – railroads, telegraph, telephone, automobiles, airplanes, television: all revolutionary ways to connect things faster – but how many had made investors rich? There were 2000 auto companies in the first half of the 20th century, but as of a few years ago, only three car companies survived in the United States.“

At the time of writing, there are currently 2,269 distinct cryptocurrencies being listed in CoinMarketCap, 949 different cryptocurrencies have already failed to date and many of the projects are expected to follow suit.

Unlike conventional cryptocurrencies, the strength of Facebook’s core business model of online advertising provides investors with an adequate margin of safety even under the scenario where Project Libra fails to see the light of day. This is a favourable investment opportunity for value investors to gain exposure to the blockchain industry without risking a permanent loss of capital.

Author: Roger Teoh

{kind=link}